Macro Economic Outlook (MEV) 2012

Economic picture uncertain

Economic picture uncertain

According to the Macro Economic Outlook 2012 (MEV 2012), published by CPB Netherlands Bureau for Economic Policy Analysis today, the Dutch economy is projected to grow by 1½% during 2011 and by 1% during 2012. The economic growth is largely attributable to exports. At this moderate rate of growth, unemployment will not decrease any further and is projected to stabilise at an average of 4¼%. Purchasing power will decrease in both forecast years. The forecasted budget deficit is diminishing rapidly, from 5.1% of gross domestic product (GDP) in 2010 to 2.9% of GDP next year. This relatively sombre picture is considered the most likely scenario based on current information, and hence the picture on the basis of which the budget has been prepared (the ‘baseline’).

These figures have taken into account the recent turmoil in financial markets, although not the possibility of a new financial crisis. The risk of a new financial crisis is nonetheless very real. The turbulence in financial markets indicates the existence of great uncertainty and the likelihood of a negative outcome is considerable. The Macro Economic Outlook 2012 therefore includes an alternative scenario in which the possible effects of a new financial crisis are illustrated. The uncertainties are too great and diverse for this to constitute a detailed scenario, however. It does give an indication nonetheless of the possible outcomes in the event a new shock, which has not yet been factored in at this moment, is delivered to the financial markets - whether in Europe, the United States or elsewhere.

| 2010 | 2011 | 2012 | |

|---|---|---|---|

| Relevant world trade volume (%) | 11.1 | 4 1/4 | 3 1/2 |

Gross domestic product (GDP, %) | 1.7 | 1 1/2 | 1 |

| Private consumption (%) | 0.4 | 0 | 1/4 |

| Gross fixed investment, private non-residential (%) | -1.4 | 9 1/4 | 3 1/4 |

| Exports of goods, non-energy (%) | 12.8 | 6 1/2 | 3 3/4 |

| Consumer prices (CPI, %) | 1.3 | 2 1/4 | 2 |

| Contractual wages market sector (%) | 1.0 | 1 1/2 | 2 |

| Purchasing power, median, all households (%) | -0.4 | -1 | -1 |

| Unemployment rate (% labour force) | 4.5 | 4 1/4 | 4 1/4 |

| Employment (labour years, %) | -1.6 | -1/2 | -1/4 |

| General government financial balance (% GDP) | -5.1 | -4.2 | -2.9 |

The signals are flashing red for the global economy. In the highly developed economies, the slowdown of the growth rate was most pronounced in the first half of 2011 due to the increased uncertainty on the financial markets, budgetary reorganisation, the high oil price and the earthquake in Japan. These are compounded by the fact that the growth in imports in emerging markets is declining due to monetary tightening and capacity bottlenecks. Global GDP is projected to grow by 3½% during 2011 and 2012, compared with 4¾% during 2010. This will result in a substantial slowing down of the export growth rate for the Netherlands.

The Dutch economy

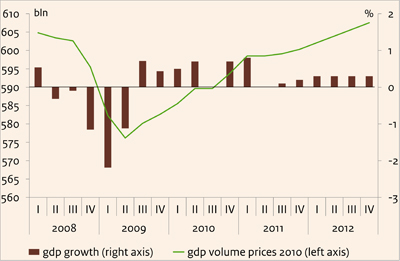

The most recent insights suggest that GDP in the Netherlands will grow by 1½% during 2011 and by 1% during 2012, significantly below the average of the previous 20 years (2¼%) and also below the potential growth rate of 1¾% forecast in the Economic Outlook 2011-2015. GDP in the Netherlands will not return to pre-credit crisis levels until the second half of 2012, meaning that the economy has merely been marking time for a period of almost four years. Dutch economic growth is dampened somewhat by the austerity measures and tax increases introduced by the cabinet (in particular in 2012), but is affected chiefly by the impact of the worldwide slowdown in growth that commenced in early 2011. The estimate has taken into account the impact of the substantial turbulence in financial markets that erupted at the beginning of August. The possibility of a new financial crisis has not been taken into account in the baseline, although such a scenario certainly cannot be ruled out.

Growth comes from exports

Economic growth in the Netherlands will come largely from exports in 2011 and 2012, with domestic expenditure only making a limited positive contribution to growth of ¼ to ½% point per year. Dutch consumers are feeling the after-effects of the crisis (loss of purchasing power, lost assets) and overall will not make any contribution to economic growth during 2011 and 2012. Public spending will inhibit the GDP growth rate next year. In the past four decades, public spending has only made a negative contribution to growth on one previous occasion, in 2004. The negative impact of public spending is not surprising given the extensive austerity measures introduced by the cabinet. Following a sharp decline in 2009 and a further decrease in 2010, business investments are projected to recover well in 2011, with a growth rate of 9¼%. This will not go all the way to offsetting the loss sustained in the previous years, however. Due to the fall off in economic activity in 2012, a decline in the growth of investments to 3¼% is once again anticipated for the coming year.

Government finances are improving, partly due to policy.....

In spite of a renewed slowing of growth, the public deficit will diminish further next year, chiefly due to austerity measures and tax increases. The deficit will decrease from 5.1% of GDP in 2010 to a projected 2.9% of GDP in 2012. This means that the deficit will have halved compared with the level in 2009 and will be below the ‘Maastricht’ ceiling of 3% of GDP for the first time since 2008. A relatively large part of the austerity measures will affect social security expenditure next year. Healthcare costs will continue to increase, albeit at a lower rate than in previous years. The tax and premium burden will increase in the projection period, from 38.8% of GDP in 2010 to 39.2% in 2012. This increase is entirely due to the effects of government policy and contributes to the reduction of the deficit.

The European debt crisis does not have any noticeable direct impact (for the time being) on the public deficit in the projection period. The bilateral loan to Greece is financed by the issuing of Dutch government bonds, thereby resulting in more interest payments for the Dutch Treasury. However, these additional interest payments are more than compensated by the interest payments made by the Greek government on the bilateral loan. Indirectly there are effects, both positive and negative, on the public deficit. The turbulence in Europe has led to investors taking refuge in bonds of strong eurozone countries, such as Germany and the Netherlands. This has resulted in downward pressure on the interest payments by the government and hence to a reduction of the public deficit. The increased uncertainty also puts pressure on economic growth, however, which is bad for government finances.

.... purchasing power in 2012 is deteriorating due to policy

Inflation, which at 1.3% was still limited in 2010, is projected to be 2¼% in 2011 and 2% in 2012. The increase in inflation during 2011 is largely due to higher import prices. In 2012 domestic factors, such as rising housing rents, gas prices, indirect taxation and unit labour costs, in particular will push up the general price level. The increase in contract wages in the private sector is forecast to rise from 1.0% during 2010 to 1½% in 2011 and to 2% in 2012. Contractual wages develop with a lagged response to the increase in inflation and the reduction in unemployment.

During 2011, purchasing power will decrease by an average of 1%, mainly because wages lag behind price movements. As a result of austerity measures and tax increases (and in the case of pensioners, the non-indexation of supplementary pensions), purchasing power will deteriorate during 2012 by an average of 1%. A change of -0.4% in 2010 means that the median purchasing power will then have decreased by roughly 2½% since 2009. This is the first time since the early 1980s that purchasing power has decreased in several successive years.

Related publications:

Short-term forecasts September 2011

The Macro Economic Outlook 2012, ISBN 978-90-1257-422-8, can be ordered from September 23, 2011 at:

Sdu Service Centre Publishers

www.sdu.nl

P.O. Box 20014

2500 EA The Hague

The Netherlands

Telephone : +31-70-3789880

Price: 28,60 euro

Read the accompanying press release.

An English translation of Chapter 1 is attached.

Related publications:

Short-term forecasts September 2011

The Macro Economic Outlook 2012, ISBN 978-90-1257-422-8, can be ordered from September 23, 2011 at:

Sdu Service Centre Publishers

www.sdu.nl

P.O. Box 20014

2500 EA The Hague

The Netherlands

Telephone : +31-70-3789880

Price: 28,60 euro

Downloads

Effecten stimuleringspakket

We are sorry, unfortunately there is no English translation of this page.

Authors

Arbeidskosten per eenheid product (MEV 2012)

We are sorry, unfortunately there is no English translation of this page.

Authors

Aspecten winstgevendheid bedrijven (MEV 2012)

We are sorry, unfortunately there is no English translation of this page.

Authors

CPBs short-term forecasts September 2011: Economic picture uncertain

- Main Conclusions

- The table 'Extended main economic indicators'

- Graph 'Economic growth in the Netherlands, 2008-2012'

- Related Publications

- Appendix : Main Economic Indicators for the Netherlands, 1970-2012

- Appendix : Main indicators labour market, 1970-2012

Main conclusions

Read the accompanying press release.

The table 'Extended main economic indicators'

| 2009 | 2010 | 2011 | 2012 | |

|---|---|---|---|---|

| Relevant world trade (vol. %) | -13.4 | 11.1 | 4 1/4 | 3 1/2 |

| Import price goods (%) | -7.3 | 7.3 | 7 | -1/2 |

| Export price competitors (%) | -4.8 | 7.7 | 3 | 0 |

| Crude oil price (Brent, $) | 61.5 | 79.5 | 110 | 106 |

| Exchange rate (dollar p euro) | 1.39 | 1.33 | 1.42 | 1.43 |

| Long-term interest rate (level in %) | 3.7 | 3.0 | 3 1/4 | 3 1/4 |

| 2009 | 2010 | 2011 | 2012 | |

|---|---|---|---|---|

| Gross domestic product (GDP, economic growth) (%) | -3.5 | 1.7 | 1 1/2 | 1 |

| Value gross domestic product (GDP) (bln euro) | 571.1 | 588.4 | 605 | 623 |

| Private consumption (%) | -2.6 | 0.4 | 0 | 1/4 |

| Public demand (%) | 4.8 | 0.7 | 0 | -1 1/4 |

| Gross fixed investment, private non-residential (%) | -12.4 | -1.4 | 9 1/4 | 3 1/4 |

| Exports of goods (non-energy) (%) | -9.3 | 12.8 | 6 1/2 | 3 3/4 |

| of which domestically produced (%) | -10.5 | 9.4 | 2 1/2 | 2 |

| re-exports (%) | -8.2 | 15.8 | 9 3/4 | 5 |

| Imports of goods (%) | -9.7 | 12.6 | 6 1/4 | 2 3/4 |

| 2009 | 2010 | 2011 | 2012 | |

|---|---|---|---|---|

| Export price goods (excluding energy) (%) | -5.2 | 4.4 | 2 1/2 | 0 |

| Price competitiveness (%) | 1.9 | 1.8 | -1 1/4 | 3/4 |

| Consumer prices (CPI) (%) | 1.2 | 1.3 | 2 1/4 | 2 |

| Consumer prices (harmonised, HICP) (%) | 1.0 | 0.9 | 2 1/2 | 2 |

| Price of gross domestic product (%) | -0.4 | 1.3 | 1 1/4 | 2 |

| Price of national expenditure (%) | 0.7 | 1.4 | 1 3/4 | 2 |

| Contractual wages market sector (%) | 2.7 | 1.0 | 1 1/2 | 2 |

| Compensation per full-time employee market sector (%) | 2.2 | 1.5 | 3 1/4 | 3 1/2 |

| Gross wage Jones family (in euro's) | 32500 | 32500 | 32500 | 33000 |

| Purchasing power (Jones, one-income household) (%) | 1.8 | -1.3 | -1 1/4 | -1 1/2 |

| Purchasing power (median, all households) (%) | 1.8 | -0.4 | -1 | -1 |

| 2009 | 2010 | 2011 | 2012 | |

|---|---|---|---|---|

| Population (x 1000 pers.) | 16530 | 16615 | 16690 | 16765 |

| Labour force (15-74) (x 1000 pers.) | 8772 | 8748 | 8700 | 8730 |

| Employed labour force (15-74) (x 1000 pers.) | 8445 | 8358 | 8335 | 8355 |

| Unemployment (x 1000 pers.) | 327 | 390 | 365 | 375 |

| Employed Persons (15-74) (%) | -0.7 | -0.3 | 1/4 | 1/4 |

| Labour force (15-74) (%) | 0.7 | -0.3 | -1/2 | 1/4 |

| Employed labour force (15-74) (%) | 0.1 | -1.0 | -1/4 | 1/4 |

| Unemployment rate (% labour force) | 3.7 | 4.5 | 4 1/4 | 4 1/4 |

| Idem, national definition (% labour force) | 4.8 | 5.4 | 5 | 5 1/4 |

| 2009 | 2010 | 2011 | 2012 | |

|---|---|---|---|---|

| Production (%) | -5.1 | 1.3 | 2 1/4 | 1 |

| Labour productivity (%) | -2.9 | 2.9 | 3 | 1 1/4 |

| Employment (labour years) (%) | -2.2 | -1.6 | -1/2 | -1/4 |

| Price gross value added (%) | 2.5 | 2.2 | 0 | 1 1/2 |

| Real labour costs (%) | -0.3 | -0.6 | 3 | 2 |

| Labour share in enterprise income (level in %) | 81.1 | 78.7 | 78 3/4 | 79 1/4 |

| Profit share (of domestic production) (level in %) | 7.6 | 7.8 | 8 1/4 | 7 1/2 |

| 2009 | 2010 | 2011 | 2012 | |

|---|---|---|---|---|

| General government financial balance (% GDP) | -5.6 | -5.1 | -4.2 | -2.9 |

| Gross debt general government (% GDP) | 60.8 | 62.9 | 64.6 | 65.6 |

| Taxes and social security contributions (% GDP) | 38.3 | 38.8 | 38.6 | 39.2 |

Economic growth in the Netherlands, 2008-2012